Extreme Avoidance

I read a story in the New York Times (I am now a subscriber, at least temporarily) with the headline

Student Debt Burdened Them, So They Moved Abroad and Stopped Paying

Whoa, says I. Did not occur to me that was a way to avoid any debt. I mean, if they can’t find you they can’t collect, and a good way to be hard to find is to move to another country, that I can see. But this seems a drastic step to take, and I’m pretty sure it does not actually wipe out the debt, so going back to the US ever would be off the table.

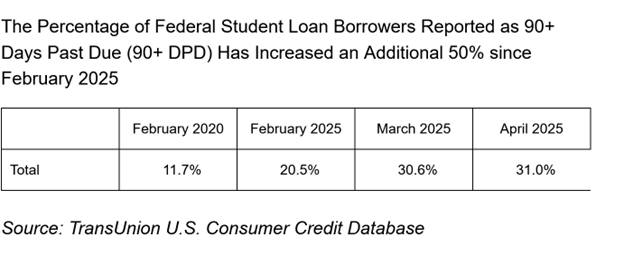

Before I get to the NYT article on this, I thought I should go looking for some general facts about US student loan defaults. I did, and found the graphic below:

90 days past due is not technically in default, I believe, but it is the step just before default. And clearly the percentage of these loans at that stage is much higher than it was just before the Covid Catastrophe. So, OK – things have changed for the worse in those 5 years. I could not find any more current numbers, but 30+% at 90+DPD seems like a big number to me.

As to the NYT article, the first thing it does is quote one Amanda Lynn Tulley, who moved to Prague a year after graduating with a Master’s degree in historic preservation from the U of Oregon. She has not made a loan payment in over 7 years – way more than 90 days.

The quote from the story:

“I was never financially stable because I was never taught to be financially stable,” Ms. Tully, 37, said.

Ah. It’s mum and dad’s fault. I should add that Ms Tully is taking a beating on social media, according to a story in the New York Post, because of that quote, and because it turns out that the payment she went to Prague to avoid was $60/month.

NYT likes telling personal stories, as do most media these days, and in the article is also featured one Eric Cooper. He graduated with a degree in logistics and $60k in student debt, but got a job right away paying $50k/year, so the repayment amount was leaving him in tough financial shape. Easy to see why, since his pre-tax income would have been just over $4k/month, meaning maybe $3k and a bit per month take-home.

He took a different tack. His loan was through his parents, so he knew that if he bailed on it, they would be responsible for repayment. He therefore consolidated the loan into a personal loan in his own name, moved to Southeast Asia to teach English and continued making minimum payments while applying for citizenship in his new country. He stopped paying when he got citizenship in 2019.

However, the last word in the article goes to one Michele Zampini, associate vice president of federal policy and advocacy at the Institute for College Access and Success.

Here is the last two paragraphs of the NYT article, all from Ms Zampini:

Ms. Zampini said she was concerned about the narrative that defaulted borrowers living abroad were “gaming the system,” or being such a small minority of borrowers that their experiences shouldn’t motivate policy change.

“This is one piece of the bigger puzzle of how borrowers are managing,” she said. “The fact that someone would need to make such a drastic life change driven by student debt is, itself, an indictment of a broken system.”

Yes. That a borrower would leave the country to avoid a $60/month loan payment surely shows that it is the system that is broken.

From the mouth of a VP of policy and advocacy to your ears.