Poor France…..Poor Us?

Here comes another article prompted by something I read in the WSJ, this time an editorial titled ‘Who Can Save France Now?’ credited to The Editorial Board.

France has a hybrid governmental structure. There is a President, currently Emmanuel Macron, who is elected in a separate election, just as in the US. However, they also have a parliamentary legislative branch, headed by a Prime Minister, who must command the confidence of that legislature to stay in office, just as in Canada and the UK. Well, the PM in France, Francois Bayrou, lost a confidence vote by a count of 364 to 194 (i.e., not close) and so Mr. Macron, whose position is unaffected by this, has two choices. He can call new legislative elections, as in Canada, or he can try to find another schmuck to appoint as PM and hope that person can put together a program which will win him/her the confidence of the current legislature.

Here’s the WSJ EB’s take on the situation:

This fiasco isn’t Mr. Bayrou’s fault. To him fell the unenviable task of crafting a government budget plausible enough that everyone could pretend to believe it. France’s debt-to-GDP ratio is due to climb to 116% this year, and annual government expenditure is approaching 60% of GDP.

The National Assembly is split among three factions—Mr. Macron’s centrists, and big-spending parties on the left and right. Actual spending cuts are out of the question politically. Mr. Bayrou hoped he could at least corral lawmakers behind an agreement to slow (ever so modestly) the rate of increase in future spending. Apparently not.

The question this brought to my mind was: is France’s fiscal position really so perilous? What does a debt to GDP ratio of 116% mean, and how does it compare to other countries?

First, one way to characterize what it means is this. GDP is the total value of everything produced in a country in one year. Government debt, which is what is meant here, is the total value of all French government bonds held by anybody. So, the 116% means that if France consumed nothing for a year (impossible, of course) and spent all the money they earned from producing things in that year on paying off their government’s outstanding bonds, there would still be outstanding debt they could not pay off. They would have to devote another 16% or so of next year’s production revenues to retire the remaining debt, assuming their government did not borrow anymore.

That sounds like a lot of debt when you put it that way, but how does it compare to other countries?

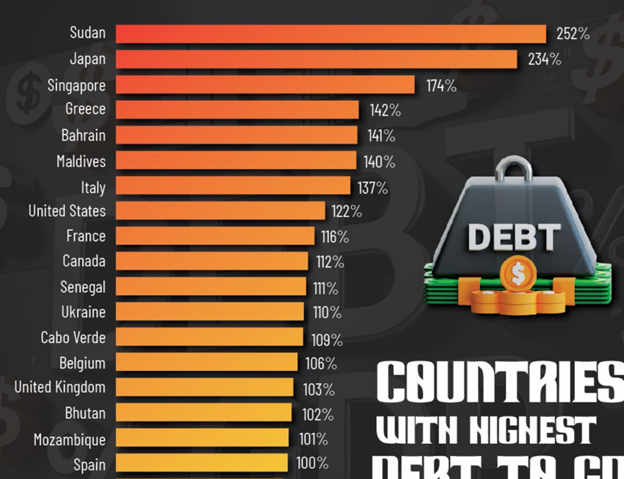

I found the graphic below online, depicting the top debt-to-gdp ratio countries in the world, based on data from the International Monetary Fund, a generally reliable source.

Apparently France has the 9th-highest govt debt to gdp ratio in the world, but it is half that of Japan, which seems to be ticking along ok, and it is less than that of the US and just ahead of Canada. Now, the conventional wisdom is that the US is able to get away with loads more government debt than other countries because the US dollar is the currency in which the vast majority of international trade is conducted. This makes everyone more willing to hold US bonds than those of other countries. But if France is in trouble on this score, what about Japan and Canada, never mind Italy?

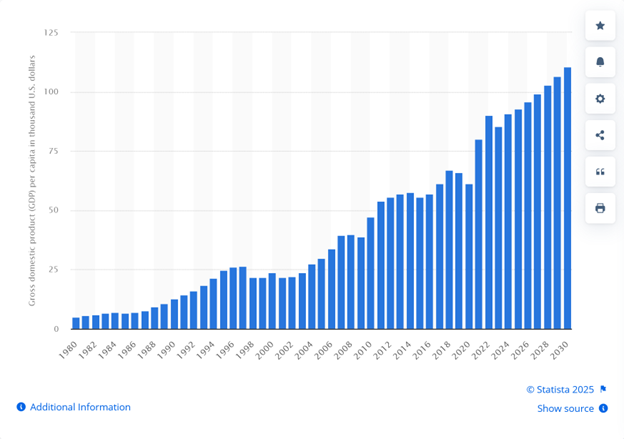

Sudan, at the top of the chart above, has been at war for as long as I can remember, and there is nothing like military conflict to run up government spending. But number three on this chart is Singapore, which I always thought of as an economic success story, even though nothing on earth would get me to live there. Well, below is the historical record of Singapore’s GDP per capita, which, flawed thought it is, is the best measure of material well-being for a country we have.

I wouldn’t take too seriously the numbers after 2024, those are projections (otherwise known as guesses), but up to last year, the Singaporean economy seems to have been doing well for its people. And, if nothing else, the guesses past 2024 suggest that the guessers don’t see Singapore’s current 174% govt debt to gdp ratio being a hindrance to a growing economy.

I suspect the Wall Street Journal EB is just not happy about a country that is racking up debt and getting away with it. They often rail against the US government, independently of who is in office, on the same grounds, and would probably do the same to Canada if they ever bothered about Canada at all.

I share their disdain for the idea that governments can borrow forever with no consequences, but the fact is that plenty of governments have been doing it for a long time, and no one knows where it will end up. The world’s governments are, in my view, jointly embarked on a long-run uncontrolled experiment in indebtedness. My concern is that if it turns out badly, none of Misters Macron, Bayrou, Trump or Carney will pay the price: it will be, as always, Joe and Jane Average who do.